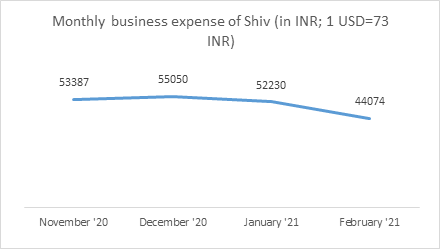

7th March 2021: A vicious cycle of income and business expenses

Shiv, one of our diarists, runs a shop in Kolkata from which he sells snacks, cosmetics, and food items.

His shop is Shiv’s only source of income. Before COVID-19, he would earn INR 15,000 a month on average as net income from the shop. During the harshest months of the COVID-19 pandemic in 2020, his earnings fell to INR 8,000 a month. At the time of reporting, his income is yet to reach the levels from before the pandemic. In February 2021, Shiv’s total income was INR 5,670/-.