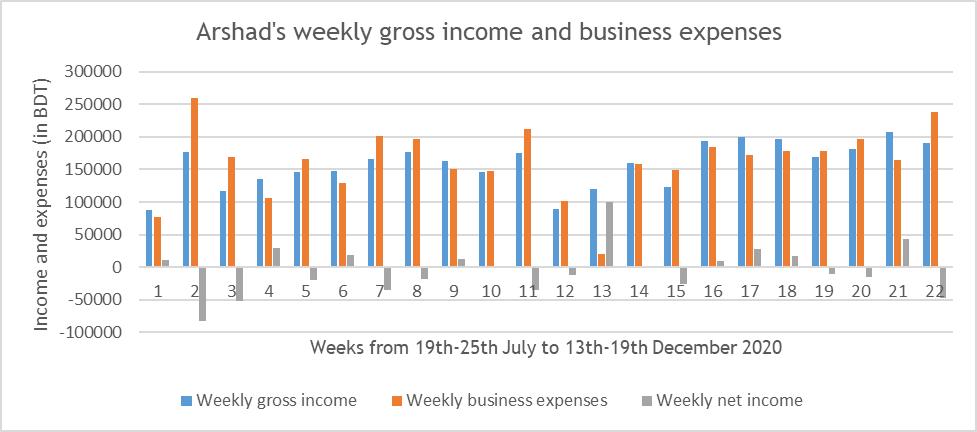

When we asked Arshad about these losses, we got an interesting reply. He revealed that he does not track his weekly income and expenses carefully and was not aware that he was incurring losses in many weeks. Before the diaries started, he did not keep detailed records of income and expenses. Even now, he records these details for the project but does not use them to plan his business.

Instead, Arshad tries to lower his business expenses by buying stock before prices go up. As a result, he makes losses in those weeks when he buys stock in bulk. Arshad is not worried about making profits some weeks and losses in other weeks. “This is all part of the game and things will be alright in long run”, he notes, smiling.

How did he manage his household expenses in these tough times? Like many low-income households, Arshad has more than one stream of income. His wife is a government high school teacher, and her income takes care of some of the family expenses. Arshad’s household is part of a joint family—he lives with his elder brother’s family. One of his nephews works in Singapore and the remittances he sends helped the household during the peak time of COVID-19 and even now.

Arshad was fortunate that his household had several regular sources of income, unaffected by the pandemic. This reemphasizes the importance of regular guaranteed income in situations like COVID-19—be it through a secure job or direct cash transfer. Fortunately, both the Government of Bangladesh and BRAC, the largest NGO in Bangladesh, ran cash transfer programs for the poor in the country and these programs helped millions of households to survive the pandemic.

The pandemic has not changed the way Arshad runs his business. Operating the business in the early morning hours was a temporary coping strategy and Arshad discontinued this once the lockdown was eased. He chose not to digitize his business operations. His customers mostly pay him in cash, and most people in the locality do not have the means to buy digitally.

Among the 60 diarists of the Hrishipara Diaries project, none has a debit card, credit card, or other means to make digital payments. Though some use mobile money services (MFS), they do not use it to purchase goods at shops. In his dealings with suppliers, Arshad rarely uses DFS for payment because the suppliers, who must pay fees to withdraw the payments see it as an expensive option.